Table of Content

You must also have an eligible military service history in order to use the VA loan program. However, you’re not required to cash out home equity with this loan. You can also use a VA cash-out refinance to replace a non-VA loan with a VA loan and lower your mortgage interest rate. Together, they’ll work with you to discuss different loan options to see what option fits best for your short-and long-term goals. Buying a home is a fun and exciting milestone – but we know there are tons of questions – and that’s okay!

You must also live in the home that is being refinanced. The VA cash out refinance loan is a mortgage refinance loan that replaces your current mortgage with a new one. However, instead of just replacing it, the new loan is for a larger amount so you can gain access to a portion of your equity.

Am I eligible for home repair assistance?

It can pay for necessary changes to your relative’s home. A .gov website belongs to an official government organization in the United States. In this short video listen to what Veterans say what "Home" means to them.

Whether it’s your first home, a vacation getaway, or an investment property, we’ll help you get there. To learn more about LIHEAP, see the program’sfrequently asked questions list. On average, about 20% of households that are qualified for LIHEAP receive benefits. When LIHEAP funds run out for the year, no more benefits can be given until Congress makes more funds available. Learn if you may be eligible for WAP and, if so, how to apply. Utilities will come out to mark the area to help you avoid damaging or being injured by underground utility lines.

Request your Certificate of Eligibility (COE).

Income has to be verifiable, reliable and ongoing for a lender to approve your mortgage. I just closed on my house and used a fantastic lender at USAA. I’m also a Remax Realtor that specializes in working with Veterans. I have been living on a military program called VASH which parteners with HUD. Go to any VA-approved lender and ask them to check your eligibility.

Mortgage loans are arranged with third-party providers. In New York State it is licensed by the Department of Financial Services. Please click here if you do not wish us to sell your personal information. The VA could allow you to borrow against all of your home value. In lender-speak, this means you can get a loan with 100% loan-to-value . But just because the VA is OK with 100% LTV doesn’t mean your lender will be.

Cool Home Equity Loans For Veterans References

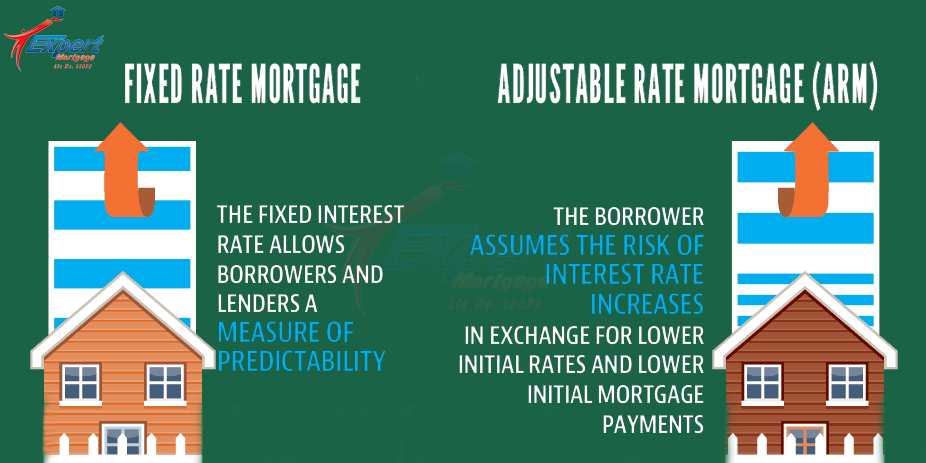

VA loans are advantageous in that there is no down payment required and no mortgage insurance. However, VA loans are not open to everyone, as you’ll need to have some form of qualifying military service. With a 10% down payment, FHA allows credit scores as low as 500. If you don’t have 10%, you’ll need at least a credit score of 580 for the minimum 3.5% required down payment. Your lender considers several factors when deciding on your interest rate, including credit score and the amount borrowed.

Compared to many other types of loans, conventional loans often provide the most competitive rates and fees. There is no minimum credit score required, but the VA requires lenders to evaluate income and monthly debts to determine if borrowers can make monthly payments. The only VA loan option that allows you to cash out home equity is the cash out refinance program.

VA Home Loans

This system can provide borrowers more flexibility than a traditional home equity loan. Seven Department of the Navy employees founded NFCU in 1933 to help themselves, co-workers, and family members achieve financial goals. In particular, these founders imagined a credit union offering loans with affordable rates and reasonable terms. NFCU has opened its membership to all military members, veterans, Department of Defense employees, and their families.

Using a VA loan saves you money upfront, and tremendously increases your buying power. Second, they may think getting a VA loan is an arduous process to be avoided. Last, some lenders don’t take the time to teach Veterans about the program, or don’t know much about it themselves.

You just won’t receive the guarantee of a VA-backed loan on this new loan. Turn your home equity into cash and reduce your mortgage rate at the same time. If you owed $100,000 on your mortgage but your house was worth $200,000, you’d have $100,000 in equity reserves.

With a VA Cash-Out refinance, qualified homeowners can typically borrow up to 90 percent of their home's value. Borrowers are subject to market rates because it's a new loan. You may need a smaller amount of money or don’t wish to use your home as collateral.

Conventional loans, the most popular choice, require as little as 3% down. For borrowers who do not qualify for a conventional loan, an FHA loan is a common alternative, requiring as little as 3.5%. The good news is that the VA cash-out refinance can be opened for up to 100 percent of the home’s value. The VA program can refinance a loan to a lower rate even if the homeowner is nearly underwater. The veteran can use a VA cash-out loan to refinance the FHA mortgage into a VA one — even if they do not want to take additional cash out. The veteran now has a no-mortgage-insurance loan and, potentially, a new lower rate.

Veterans can access all the typical home equity financing that civilians have and more. We cover some of the best options for veteran homeowners. However, the interest on a home equity loan is just one of the costs involved with taking out a home equity loan.

Home equity loan fees may be similar or identical to the fees you paid for your original mortgage. You should expect to pay about 2% to 5% of the loan amount in fees and closing costs. There are different ways to access capital, but all require that the home have enough equity to warrant a refinance loan. You also must meet all credit and income requirements to get the refinance. VA typically charges a funding fee to defray the cost of the program and make home buying sustainable for future Veterans. The fee is between 0.50 percent and 3.3 percent of the loan amount, depending on service history and the loan type.

No comments:

Post a Comment